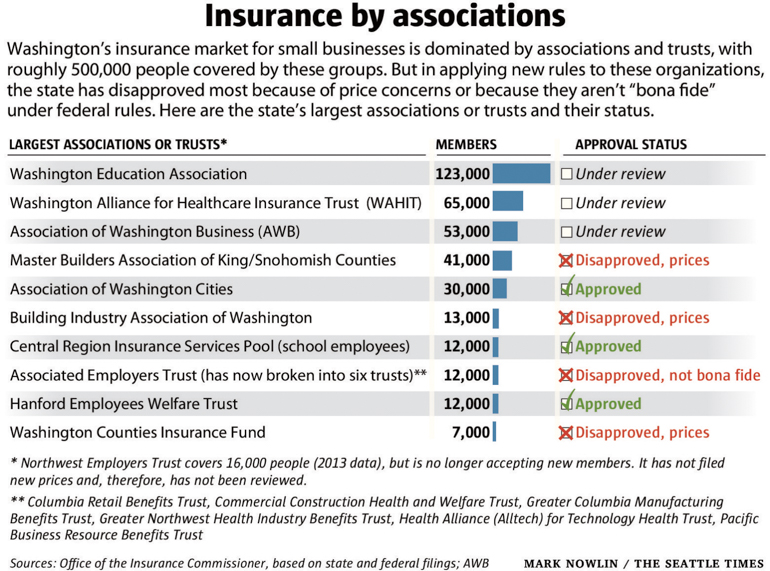

But while the Washington Education Association (WEA) health trust won approval, dozens of other associations and trusts with plans covering hundreds of thousands of small-business employees and their households have either been denied or are in limbo, awaiting a decision. Of Washington state’s more than 60 association and trust plans, 11 are approved, nine are under review and the rest have been rejected.

Mounting frustration with the process has caused association-plan backers to run full-page newspaper ads and lobby state lawmakers to protest Kreidler’s actions. Many are challenging the Office of the Insurance Commissioner (OIC) in court or through administrative hearings.

Kreidler asserts that the Affordable Care Act brought into play new rules that affect association health plans, changing which businesses can buy insurance through different trusts and reshaping the way the insurance is priced. Associations counter that Kreidler is misinterpreting the law.

Associations and trusts for years have been the most popular insurance option for Washington’s small employers because their products generally were cheaper than the health insurance available on the open market. That resulted in part from the plans’ ability to charge businesses with sick workers more money, a practice no longer allowed under the ACA.

“Associations offer a lot of benefits to their members, and to their communities. We’ve worked very hard to reach out to as many associations and insurers as possible for the last several years to help them understand the new federal law,” Kreidler said in a statement.

For the WEA’s health association, the review went smoothly.

“Our pool [of covered employees] has remained stable, so we haven’t had to make any changes,” said Linda Mullen, director of communications at the WEA. “It’s the same people we’ve been covering for 40 years.”

For others, it hasn’t been so easy. The insurance commissioner’s office says associations need to clear two bars for approval. First, they must cover businesses in the same sector as the associations, such as car dealers or farmworkers. Then, they must price their insurance in a way that meets the new rules, which generally means prices can vary — within prescribed limits — by age and geography. They cannot vary by sex.

An insurance department analysis of recently proposed rates found that in some cases, older workers and women of reproductive age were being overcharged in association plans.

The Health Alliance for Technology (ALLtech) trust, which provides insurance for 110 smaller technology companies, missed both marks when it was reviewed, and it’s appealing the decision.

Before the ACA kicked in, “we went with our arms wide open” to the insurance commissioner to try to set up a product that would meet the new rules, said Ken Myer, the trustee providing fiduciary oversight at ALLtech.

The companies using ALLtech plans are “competing for talent with some of the bigger players in the industry,” Myer said. They need to be able to offer plans with rich benefits that at least approach what’s offered by large employers, and ALLtech helped them do that, he said.

The state review process has gone more slowly than expected, and the office is still issuing decisions for plans started in 2014, some of which still could be in effect. All the 2015 plans are pending review.

None of the workers covered by disapproved plans have lost their coverage, said Stephanie Marquis, an insurance department spokeswoman. The trusts have 90 days to appeal the decisions and many have. If they do not, the department has offered to help the trusts transition employees to approved plans.

The Washington Counties Insurance Fund trust, which covers 7,500 county workers plus employees working at fire, hospital and library districts, was rejected because of its prices. Jon Kaino, executive director, said the rates had nothing to do with workers’ health, and he can’t understand the ruling.

In fact, Kaino argues that the trust’s prices are fairer than what’s offered on the open market. Under the ACA, insurance prices can increase each year as a person gets older. The county trust instead takes the average age of all an employer’s workers and sets the rate there. That way, insurance for a 60-year-old employee costs the same as for someone who is 30.

The solution is simpler for bookkeeping and could discourage an employer, who pays much of the insurance costs, from discriminating against older workers, Kaino said. On charging individuals according to age, he said, “it’s incentivizing age discrimination, and we don’t do that.”

Marquis didn’t know exactly why the county trust failed the pricing test. The insurance department asks trusts to explain why one group is being charged more than another, and sometimes the trusts haven’t provided enough information to explain it.

“We just believe we’re enforcing the federal law as written,” Marquis said.

Kaino’s trust is to argue its case before an administrative hearings officer later this month, and he’s optimistic: “I believe we can win.”

Â鶹ŮÓÅ Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at Â鶹ŮÓÅ—an independent source of health policy research, polling, and journalism. Learn more about .This <a target="_blank" href="/insurance/small-business-employees-group-slams-washington-state-for-rejecting-health-plans/">article</a> first appeared on <a target="_blank" href="">Â鶹ŮÓÅ Health News</a> and is republished here under a <a target="_blank" href=" Commons Attribution-NonCommercial-NoDerivatives 4.0 International License</a>.<img src="/wp-content/uploads/sites/8/2023/04/kffhealthnews-icon.png?w=150" style="width:1em;height:1em;margin-left:10px;">

<img id="republication-tracker-tool-source" src="/?republication-pixel=true&post=541161&ga4=G-J74WWTKFM0" style="width:1px;height:1px;">]]>{kind=link}

For 20 years, small businesses in the state have relied heavily on associations and trusts to provide coverage for their workers. These groups had cheaper prices than insurance sold on the open market, allowing them to become the dominant players, with roughly half a million of the state’s residents covered by these plans.

Now Insurance Commissioner Mike Kreidler, citing federal changes under the ACA, has rejected the majority of the state’s roughly 64 association and trust plans, saying they don’t comply with the new rules.

Kreidler said the changes will create a fairer, more stable marketplace in the long run for small-business coverage. Based on an Office of the Insurance Commissioner analysis of association plan prices for 2015, some employees are getting a raw deal, the commissioner said, with older workers sometimes paying eight times more than younger workers, and women of childbearing age paying higher rates, too.

Association proponents say the system is popular and works well, and they’ve challenged Kreidler’s policies, arguing that he has no legal power to disapprove their plans. Even those who don’t entirely object to Kreidler’s overhaul say the rollout of the rules and the review of the plans have been a disorganized, ad hoc mess.

As a result, health-insurance coverage for many small employers and their workers hangs in limbo — though most people likely don’t even know it.

“They are the innocent victims here,” said Sean Corry, a Seattle insurance broker with dozens of clients with association plans. “It’s all very irritating. I can’t tell our clients what’s going to happen. I can’t tell them they can keep their plan” a whole year.

Small businesses have traditionally had two insurance options: the small group market, which is open to everyone, or associations and trusts. (This year a third option became available statewide, small business insurance sold by the state-run Washington Healthplanfinder exchange, but few have signed on.)

In 1995, the Legislature created special rules for associations and trusts, allowing employers with 50 or fewer workers to buy “large group” insurance through the organizations. It meant the associations didn’t have to follow small-group rules, a provision that allowed price variation from employer to employer. The associations could charge a business with sick workers higher rates, essentially forcing them out, while keeping the prices lower for everyone else.

Washington’s rules created a market for small businesses dominated by associations and trusts — perhaps more so than in any other state.

But while associations thrived, the small group market, which cannot vary prices according to someone’s health, became much smaller and more expensive. Kreidler has warned that with so much “bad risk” — employers with sicker workers — in the small group pool, it could become unviable.

“If you want to have a stable market, you have to make sure plans aren’t cherry-picking the market,” Kreidler said. The commissioner, first elected in 2000, has over the years tried to stop the associations from such “cherry-picking.” He didn’t succeed.

Then came the ACA.

Dozens of plans disapproved

The 2010 ACA includes rules for insurance marketplaces, and those, in combination with additional instructions from the federal government, have led Kreidler’s office to apply a two-part test to associations and their plans to determine if they’re operating legally.

First, the association must have been formed for a purpose other than simply selling insurance, and its members must work in the same industry, such as farmworkers, restaurants or aerospace employees. A group meeting this criteria is deemed a “bona fide” association.

The second test determines whether the association is selling insurance plans at an appropriate rate. The plans can’t charge more for sick people or women, and they are limited as to how much more they can charge older workers than younger ones.

So far, only nine plans have cleared both hurdles. Nineteen failed the bona fide test and 22 were denied because of their rates. Two trusts that were disapproved are fighting the Office of the Insurance Commissioner (OIC) through administrative hearings, and one of them also filed a case in federal court.

One of those the office denied was the Master Builders Association Health Insurance Trust, which covers approximately 1,400 companies and 40,000 workers and their families in King and Snohomish counties.

The trust tried to meet the new rules, cutting up to 12 percent of its member companies to clear the bona fide bar, said Jerry Belur, CEO of EPK & Associates in Bellevue, which administers the trust. In January, Belur learned his trust was denied because of its prices.

“We were surprised and a bit disappointed because of our close working relationship with [Kreidler’s] office and the steps we had taken to meet the requirements in order to operate like we have for 20 years,” Belur said. The organization has not challenged the decision on legal grounds.

“We see this as one more step and are hopeful that the OIC will embrace our desire to continue to collaborate,” he said.

Impact on workers

Associations with disapproved plans have 90 days to appeal the ruling, and the employees they cover still have their insurance. If an association doesn’t appeal, the OIC asks that the group contact the agency, which can help move people to new coverage. That could include moving to another association, to the small group market, or to the state’s insurance exchange, either in the small group or individual market.

“We’ll wind up working with them so there will be a reasonable transition,” Kreidler said. “We’ll work to minimize the impact on individuals.”

An additional 13 plans await the office’s ruling; two are from the Association of Washington Business’s HealthChoice program, which insures 53,000 people.

While the AWB plans have not received the office’s approval, Jeff Gingold, an attorney representing association health plans including the AWB, said there is no legal requirement for Kreidler to sign off on their product.

Kreidler “has gone way beyond his constitutional authority, his legislative authority, even beyond his own rule making,” Gingold said. “Clearly the ACA has changed a lot of things in the health-care market, but in this particular area, Kreidler has been extremely vague as to what in the ACA has made this change.”

What may lie ahead

Gingold defends the association plans as a good deal for employers and employees, and he points out that 90 percent of enrolled employers renew their AWB coverage each year. If customers felt ripped off, Gingold said, they’d take their business elsewhere.

“Who is [Kreidler] protecting here?” he asked.

While experts are split over which side will prevail in the fight over the regulations, many agree that if the new rules survive, the associations will not.

“I think the association plan market that you saw in Washington, absent a court intervention, will not be there [in the future],” said John Conniff, a Tacoma-based attorney specializing in insurance regulatory compliance.

What would that mean for small businesses? As with other ACA-driven changes, some people would lose plans they liked and see their rates go up while others could get better deals. It would create a system that was more equitable between the associations and the small-group market.

“It’s a good thing to have everybody in the same pool and everybody plays by the same rules,” said Corry, the Seattle broker.

When it comes to insurance, if someone is getting a great deal, “it comes at the expense of somebody else,” Kreidler said. The new rules will help level the playing field.

“The ACA has been the ladder we needed,” he said, “to get that start.”

Â鶹ŮÓÅ Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at Â鶹ŮÓÅ—an independent source of health policy research, polling, and journalism. Learn more about .This <a target="_blank" href="/insurance/health-coverage-in-limbo-for-many-small-business-employees/">article</a> first appeared on <a target="_blank" href="">Â鶹ŮÓÅ Health News</a> and is republished here under a <a target="_blank" href=" Commons Attribution-NonCommercial-NoDerivatives 4.0 International License</a>.<img src="/wp-content/uploads/sites/8/2023/04/kffhealthnews-icon.png?w=150" style="width:1em;height:1em;margin-left:10px;">

<img id="republication-tracker-tool-source" src="/?republication-pixel=true&post=527016&ga4=G-J74WWTKFM0" style="width:1px;height:1px;">]]>The good news is that since the Affordable Care Act kicked in, hundreds of thousands of formerly uninsured people have coverage in Washington through the expansion of Medicaid and sale of individual health-insurance plans.

The trouble for the Washington Health Benefit Exchange, which runs the state insurance marketplace, is that too few people are buying their coverage through the Washington Healthplanfinder website, which needs to reach the enrollment targets to help pay for its operating costs.

By Jan. 25, the state was only 60 percent of the way toward its goal of selling 213,000 insurance plans in the current enrollment period, which began in November. The window for this second round of enrollments closes Feb. 15.

There are numerous reasons for the underwhelming sales. Some officials think the nationally set enrollment window was badly timed, spanning Thanksgiving and Christmas holidays, when distractions abound and pocketbooks are strained. Then there’s the challenge of enrollment closing before most people fill out their tax returns, which means many uninsured people will realize too late how much they’re being penalized for going without coverage.

In addition, enrollment projections in Washington underestimated how many residents would be eligible for Medicaid, pulling them out of the pool of potential exchange customers. In the past 16 months, the number of Medicaid enrollees has grown by nearly half a million, to 1.7 million.

Finally, many exchange customers from the first enrollment received confusing or insufficient notices about what they needed to do to renew their plans, sometimes leaving them uninsured when they meant for their coverage to continue.

That’s what happened to James Bach, of Orcas Island. Bach and his wife, Lenore, bought insurance through the exchange last year and planned to keep it. A flier from their insurance company, Group Health, assured them they would be renewed automatically. Buried in a second notice was a sentence advising that they might need to take action to renew, but it wasn’t explicit.

It wasn’t until Bach tried to use his insurance in January that he learned it had been canceled at the end of 2014.

“It’s like turning someone’s power off,” Bach said, noting that if a company is going to shut off your power, water or cable, you get repeated notices with big red letters warning you there’s a problem. “Why wouldn’t they do it with health insurance?”

Bach, who runs a software-testing business, should have received a notice from the exchange telling him to renew, but he said he never got one.

Melinda Hews, executive director of health-insurance exchanges at Group Health, said her organization was told a batch of 20,000 reminders mistakenly was not sent by the exchange before the end of the year.

Exchange officials say they are certain everyone was provided renewal information.

“There has been many fingers pointing in all directions,” Hews said. “We’re sorry for the confusion that this new process caused people.”

Everyone with exchange insurance needs to go back to his or her Healthplanfinder account and give permission to pay for the coverage, said Michael Marchand, spokesman for the exchange. It’s like a magazine subscription, he said: “It doesn’t automatically renew unless you give the system the OK to bill their card.”

If exchange customers find that their coverage was inadvertently canceled or if they had technical problems causing them to miss an enrollment deadline, they can fill out a petition to request that their plan be made retroactive to prevent any gaps in coverage.

Bach opted to take his business elsewhere.

“We decided to abandon the exchange because of this crazy thing,” he said. He also changed insurers.

“Someone’s life could actually be at stake, and people are trying to cover their butt,” Bach said.

Working with a broker in Friday Harbor, the couple found a new plan that started Feb. 1 and say they’ve have had a positive experience overall.

Nationwide, exchange enrollments seem to be going better than in Washington.

By the end of January, 9.5 million people signed up for insurance or were automatically re-enrolled in plans sold through the federally run exchange or from one of the 13 states with their own exchange site.

While the number includes people who haven’t yet paid for their coverage, it seems likely the Obama administration will meet this year’s enrollment goal of 9.1 million customers.

The Washington exchange and its partner organizations are hustling to promote coverage, and they’re shifting tactics to include messages highlighting the penalties faced by those who remain uninsured.

Most Americans must have 2015 coverage or face a penalty of $325 per adult or 2 percent of their adjusted income — whichever is higher.

The campaign is particularly targeting younger residents, who often need more convincing of the benefits of health insurance. Tuesday night, the exchange sponsored the launch party for the Sasquatch! Music Festival, a popular concert at the Columbia Gorge over Memorial Day weekend. The exchange is running ads on music websites, social media channels and by radio DJs. Public Health — Seattle & King County is doing outreach events at community colleges.

And a pro-insurance public-service announcement starring Seahawks Russell Wilson and Richard Sherman has racked up 1.8 million views since it was released in early January.

Marchand said enrollments look like they’re ticking up this first week of February — and he hopes the trend continues.

That’s because funding for Healthplanfinder comes from three sources: the exchange’s share of a 2 percent tax on all insurance premiums, a fee charged on insurance companies selling through the exchange, and from cost sharing with the state agency that manages Medicaid.

People eligible for Medicaid, which is locally called Apple Health, sign up for the program through the Healthplanfinder website.

The board overseeing the exchange is asking state lawmakers to approve a budget request of $147 million over two years, which is already higher than what the Legislature initially allocated.

Through new sales or renewals, the exchange needs to sell 86,000 plans in the last three weeks of open enrollment to reach its target and provide funding to operate within that request.

Marchand said the exchange knows lawmakers will be looking everywhere to make cuts, not grow budgets.

That could mean paring back services, he said. “We’ve got to figure out how to live within our means.”

Â鶹ŮÓÅ Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at Â鶹ŮÓÅ—an independent source of health policy research, polling, and journalism. Learn more about .This <a target="_blank" href="/insurance/obamacare-enrollment-falling-short-in-washington-state/">article</a> first appeared on <a target="_blank" href="">Â鶹ŮÓÅ Health News</a> and is republished here under a <a target="_blank" href=" Commons Attribution-NonCommercial-NoDerivatives 4.0 International License</a>.<img src="/wp-content/uploads/sites/8/2023/04/kffhealthnews-icon.png?w=150" style="width:1em;height:1em;margin-left:10px;">

<img id="republication-tracker-tool-source" src="/?republication-pixel=true&post=520160&ga4=G-J74WWTKFM0" style="width:1px;height:1px;">]]>“I felt like we hit the jackpot,” she said.

But last spring when Chase was struck with an unexpected illness, the Seattle woman was shocked to realize how little her new health insurance plan — a Health Savings Account (HSA) with a deductible of roughly $5,000 — would cover.

High-deductible and HSA plans are appealing because of their lower monthly premiums. But many consumers don’t realize how much money they’ll spend out-of-pocket with these plans through copays and coinsurance if they get sick. Despite being insured, this kind of coverage can drive people into debt or cause them to skip needed care for fear of unaffordable medical bills.

The problem isn’t likely to improve anytime soon. During the first open enrollment to purchase insurance from online health marketplaces under the ACA, more than one-third of the 150,000 individual policies sold through Washington’s Healthplanfinder exchange were “bronze” level plans with more limited coverage. The plans for 2015 with the highest deductibles will require a consumer to spend $6,600 (with some exceptions), before an insurance company starts paying the full cost of their health-care bills.

“People aren’t able to afford the copays and out-of-pockets,” said state Rep. Joe Schmick, a Republican, and ranking minority member of the House Health Care and Wellness Committee. Folks say to him: “Do I really have insurance when I have to pay this much out of my pocket? It doesn’t feel that way.”

In a recent survey of 1,004 insured Americans, more than one-quarter said they had a high-deductible plan. Almost 30 percent of them said they hadn’t gone to the doctor when they were sick because of the costs they’d have to pay, according to the poll taken by The Associated Press-NORC Center for Public Affairs Research.

The American Academy of Pediatrics this spring suggested that high-deductible plans should not be sold to cover children out of concern that some families would forgo needed care.

So far, the high-deductible plans have not resulted in more unpaid patient bills at Washington hospitals. Reports to the state’s Department of Health show that bad debt at hospitals has, in fact, decreased this year compared with last.

Health care providers are nevertheless concerned.

“It seems like the issue is growing and getting even more commonplace with the high deductibles and more out-of-pocket costs for patients,” said Karen Johnson, a spokeswoman with The Polyclinic, an organization of Puget Sound providers.

In response, Polyclinic is promoting a deferred deductible program in which patients will be able to pay their medical bills over 12 months with 1 percent interest. If they pay the bill within three months, the interest is dropped.

Johnson said Polyclinic historically has accommodated patients struggling financially, but “we want to be more upfront about it,” she said. “We want to be clear that we’re offering it” and “take the stigma out of it a little bit.”

State officials and others are trying to help people choose insurance that better meets their needs so they don’t wind up with unaffordable medical bills. During this second round of insurance enrollment, which started Nov. 15 and ends Feb. 15, the state’s insurance exchange is promoting videos and outreach materials explaining key insurance terms.

The exchange, which operates the Washington Healthplanfinder website, is encouraging people to use insurance brokers who give advice on plans. Brokers offer their services free and receive a commission from insurance companies.

“People are realizing that just because the premium was low, if they have to go to the doctor or have maintenance medication, those plans are not the best,” said Thea Feltzs, an insurance broker in Gig Harbor.

Chase and her husband are self-employed, and their income is modest enough that they qualified for a federal subsidy that lowered the cost of the LifeWise HSA insurance plan she bought through the state’s exchange. Their 7-year-old daughter is covered through Medicaid.

“I heard from the rumor mill that an HSA was the way to go because I’m self-insured,” Chase said. “I was really banking that my health would be good.”

In the spring, after experiencing memory problems and swollen joints, Chase was diagnosed with latent Lyme disease.

“Immediately it included a lot of [doctor’s] visits and a lot of medication and monthly tests and lab work,” Chase said. And most of it wasn’t covered by her plan. “Every time I walk in I pay for the office visit, which is $165 each month.”

A financial person at her doctor’s office referred Chase to Sarah Freeman, a Seattle insurance broker who helped her find a new plan for next year. At $325 a month, the Premera Blue Cross plan she found costs a little more than her current plan, but it will pay more of her bills.

For now the family can afford the higher premiums, Chase said, but “I just hope it doesn’t continue to rise.”

Despite the risks, Feltzs predicted the cheaper plans with higher deductibles will still be popular.

“I sell them all day because those plans do work for people who say they don’t go to the doctor or they rarely go,” said the broker. “They say, ‘I want to avoid the penalty [for being uninsured] and in the event that something does happen, I don’t want to break the bank.’ ”

Â鶹ŮÓÅ Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at Â鶹ŮÓÅ—an independent source of health policy research, polling, and journalism. Learn more about .This <a target="_blank" href="/insurance/skipped-care-a-side-effect-of-high-deductible-health-plans/">article</a> first appeared on <a target="_blank" href="">Â鶹ŮÓÅ Health News</a> and is republished here under a <a target="_blank" href=" Commons Attribution-NonCommercial-NoDerivatives 4.0 International License</a>.<img src="/wp-content/uploads/sites/8/2023/04/kffhealthnews-icon.png?w=150" style="width:1em;height:1em;margin-left:10px;">

<img id="republication-tracker-tool-source" src="/?republication-pixel=true&post=515018&ga4=G-J74WWTKFM0" style="width:1px;height:1px;">]]>This copyrighted story comes from , produced in partnership with KHN. All rights reserved.

In the shrub steppe of Grand Coulee on the banks of the Columbia River, Wash., the town’s two family doctors practice at an unrelenting pace, working on call every other night and every other weekend.

In the coastal town of Port Angeles, the doctor shortage is so acute that a clinic is turning away 250 callers a week seeking a physician.

George and Lynne Rudesill are two of those people. Since learning earlier this summer that their primary-care doctor in Sequim was retiring, the couple have scrambled to find a replacement. Their calls are being met with waiting lists hundreds of people long or advice to call again in a month.

“I’m going to have to drive all the way to Silverdale or Bremerton to see a doctor,” George Rudesill said, citing cities that are about 70 or more miles away from home. “This area is in a medical crisis right now.”

Rural areas have long been strapped for doctors, but now the Affordable Care Act (ACA) is further straining those limited resources. More people with insurance means more people will want to connect with a doctor — just as aging baby boomers require more care and the doctors are retiring.

But the 2010 health-care overhaul also includes measures to begin correcting policies that for decades have churned out a disproportionate number of specialists and urban doctors over rural family physicians. The ACA has funding this year for 550 residents in underserved rural and urban areas nationwide. In Washington alone, 28 primary-care doctors each year are completing their training in these communities thanks to ACA dollars, ready to practice where they’re needed most.

“It may be a real answer to many of the issues of getting primary-care physicians into underserved communities,” said Dr. Rob Epstein, of Family Medicine of Port Angeles, in an email.

Yet just as ACA initiatives are showing results, key incentives and investments to boost family medicine are scheduled to end this year and next. But there’s a chance the programs could survive. Shortly before Congress’ August recess, Sen. Patty Murray introduced legislation to save them.

Health-care providers and national organizations support Murray’s effort to expand and make permanent the residencies in underserved areas.

“Renewing it would make a big difference as to what’s possible for Washington,” said Dr. Nancy Stevens, director of the Family Medicine Residency Network at the University of Washington. “It’s much harder to get people to go into the rural places where we need them. You really need to create residency training spots that are in those areas.”

Rural docs are a rare breed. They treat everyone from wailing newborns to fading elders, setting bones, performing C-sections and shocking hearts into rhythm. They’re exalted, but sometimes exhausted, and it’s a path few doctors these days are willing to take.

For 16 years, Dr. Andy Castrodale has practiced rural medicine in Grand Coulee, a town of 1,000. He grew up on the nearby Colville Reservation, attended the UW School of Medicine and did a residency and fellowship in Spokane. Castrodale savors the idiosyncrasies and rewards of his career choice.

“I watch my own kids playing soccer or baseball and you realize you’ve delivered half the team,” he said. “I can look at people in town and know that I’m the reason that they’re alive. That’s humbling.”

Few doctors are ready to follow Castrodale. Only 3 percent of matriculated medical-school students say they plan to practice medicine in a small town or rural area, according to a recent survey by the Association of American Medical Colleges.

Why The Shortage

A double whammy has hit rural areas.

First, the shortage of primary-care doctors extends nationwide. About 34 percent of U.S. doctors practice primary and family care, while the rest are specialists. Research shows a ratio closer to 50-50 would provide better care and improve health overall.

Second, there are numerous hurdles to recruiting physicians to rural areas.

The work can be intimidating, with long hours and frequently being on call. It can be difficult for a physician’s spouse to find work in a place with limited economic opportunities. Finding a work-life balance is a struggle.

“Rural medicine can be pretty fun, but it can be quite demanding and this generation is less inclined to work quite as hard as previous generations,” said Dr. John McCarthy, assistant dean for regional affairs at the UW School of Medicine. “They don’t give up their life as readily.”

While Seattle and its suburbs have more than 11 primary-care physicians per 10,000 residents and so far are keeping pace with growing demand, in the northern swath of the Olympic Peninsula that number shrinks to fewer than eight, according to 2011 data. An area covering Grand Coulee’s Grant County as well as Chelan, Okanogan and Douglas counties has just over six — more than 1,500 potential patients per doctor.

One of the biggest challenges to boosting the rural physician workforce is the funding of residencies. Once a doctor finishes school, a supervised, three-year residency to hone his or her skills is typically required. Research shows that where a doctor does this training is a strong predictor as to where he or she will practice.

But historically, federal dollars for residencies mostly have been spent on teaching hospitals often located in cities. The newly minted doctors are working with sophisticated technology, surrounded by specialists. The notion of shifting from that environment to a rural clinic or hospital requiring much more self-reliance is daunting.

The result? More urban specialists, fewer rural family doctors.

“Do We Have To Move?”

The Rudesills were delighted when they moved to their airy, country home on the Olympic Peninsula nine years ago. There was plenty of open space for the English Springer Spaniels they raised as show dogs.

The couple, both 64, did find health care for problems including George’s heart disease and occasional outbreaks of a skin condition called rosacea, plus Lynne’s arthritis in one knee and high cholesterol.

That changed recently when their family doctor announced his retirement and as wait times to see the dermatologist began lengthening. The Rudesills are getting anxious.

“Do we have to move so we can find a doctor?” Lynne Rudesill asked.

Urgent-care clinics and the hospital ER are available and, in the absence of more primary-care doctors, that’s where many people are likely winding up. Another option is driving hours to an urban provider.

Family Medicine of Port Angeles is one of the primary-care practices the Rudesills tried, but staff there are telling 250 people a week to call back in case a space opens up.

Karen Paulsen is the clinic administrator and answers many of the upset callers.

“I feel a lot of compassion for their situation,” she said. “They’re ill, they need care.”

The practice is trying to squeeze in everyone it can. Their doctors have appointments booked every 15 minutes and work in teams with advanced registered nurse practitioners (ARNPs) and physician assistants (PAs) to share the workload.

Incorporating ARNPs and PAs into a practice is an increasingly common strategy in rural areas and elsewhere.

At Family Medicine, even the workspace is designed with collaboration in mind. The teams of providers sit in clusters of desks in a high-ceilinged open space, an arrangement where questions and discussions can flow freely and everyone is easy to find.

The group built the facility in 2009 to optimize efficiency. It’s clean, modern and inviting, but the clinic has had little success of late recruiting new doctors. Their staff situation worsened in recent months after they lost four MDs when two moved, one retired and another died.

Their dream is to create a new medical residency at the clinic — to train a doctor who might then decide to stay.

Renewed Focus On Rural

Before the Affordable Care Act, there were university, state and federal programs to encourage the production of more primary-care and rural doctors. But with the law’s new residency program comes a sharper focus on this mission.

The ACA’s Teaching Health Center program is funding 550 residents nationally, including training sites for doctors or dentists in Puyallup, Ellensburg, Yakima, Toppenish, Auburn, Spokane and Tacoma and the surrounding area. Rather than funding large teaching hospitals, the money targets smaller facilities serving rural, lower-income or minority residents including tribal members.

“It is helping to train physicians in rural or underserved communities,” Murray said, “and they’re staying there.”

Murray’s bill would extend the residency program until 2019 at a cost of $420 million. It otherwise ends next year. Additionally, Murray wants to use $75 million to fund the development of new training programs, bringing more attention to underserved sites.

The legislation — called the Community-Based Medical Education Act of 2014 — would ultimately grow the number of residency slots to 2,050 and make them permanent. By slightly cutting Medicare reimbursements at teaching hospitals, the savings would pay for the residents beginning in 2019.

The goal of these efforts is to produce more doctors like Christina Marchion.

Marchion, who grew up in Anaconda, Mont., graduated from the UW medical school, did her residency in Idaho and just finished an OB fellowship in Spokane. While a student, she spent time at a Lewistown, Mont., clinic, working alongside a rural doctor with whom she formed a connection.

This month, she’ll return to the 6,000-population Lewistown to practice alongside her mentor.

“My love of the idea of true, full-scope family medicine is greater than the insanity that it takes,” Marchion said.

She’s eager to practice in a rural setting where she can deliver babies — a perk most urban family doctors don’t enjoy. Plus, part of Marchion’s $300,000 student debt will be repaid through a loan-repayment program Montana uses to recruit providers.

Marchion can imagine staying in Lewistown for decades, but knows that another doctor recently tried to make it work and lasted only six months. All the same, she’s ready to give it a try.

“If I really believe in this,” Marchion said, “in underserved and rural medicine, this is my best shot.”

Â鶹ŮÓÅ Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at Â鶹ŮÓÅ—an independent source of health policy research, polling, and journalism. Learn more about .This <a target="_blank" href="/health-industry/rural-doctor-shortage-worsens-as-newly-insured-washington-residents-seek-care/">article</a> first appeared on <a target="_blank" href="">Â鶹ŮÓÅ Health News</a> and is republished here under a <a target="_blank" href=" Commons Attribution-NonCommercial-NoDerivatives 4.0 International License</a>.<img src="/wp-content/uploads/sites/8/2023/04/kffhealthnews-icon.png?w=150" style="width:1em;height:1em;margin-left:10px;">

<img id="republication-tracker-tool-source" src="/?republication-pixel=true&post=329299&ga4=G-J74WWTKFM0" style="width:1px;height:1px;">]]>This copyrighted story comes from , produced in partnership with KHN. All rights reserved.

The fear was this: The Affordable Care Act would give massive numbers of people new access to health care, creating a surge in demand for medical services and long waits to see the doctor.

But in the seven months since new insurance plans began kicking in, Puget Sound-area, Washington, primary-care providers so far seem to be keeping up with growing numbers of patients. The question now is, can they keep ahead of the demand as the formerly uninsured continue seeking care, and as baby boomers age and a sizable fraction of Washington’s physicians retire.

In just the past year, Providence and Swedish clinics in Western Washington report a 10 percent increase in primary-care visits. But patients are waiting only four or five days for those appointments, and specialty and urgent-care services are available the same day.

Group Health Cooperative officials say they’ve seen higher demand, particularly early in the year, when many new insurance plans took effect. Yet roughly one-third of their patients are able to get an appointment within 36 hours.

Patients at The Everett Clinic are waiting about a week to see pediatricians and family doctors, but those needing quicker care can visit walk-in clinics at all nine of their primary-care sites.

And when researchers pretending to be Medicaid patients called King County providers in April, they found a median wait time of seven days for an adult checkup — a statistic unchanged from December to April, despite an 80 percent increase in Medicaid enrollees over that time

Bothell resident Heather New got coverage at the start of the year through Medicaid, or Washington Apple Health, as it is known locally. Then she shifted to private insurance when she got a job three months later. With both types of insurance, she was able to see a doctor quickly at the HealthPoint clinic in Bothell.

In January, New learned she had diabetes, which the 34-year-old aspiring nurse is managing through diet and exercise. If she needs to see her doctor, she can get in within a few days. “If it’s an emergency, I can get in to the nurse practitioner the same day,” New said.

Technology, trade-offs

How are the doctors doing it?

Clinic officials say in some cases they’ve hired more providers, but the bigger strategy seems to be doing more with technology and with the staff they already have.

There are trade-offs. Patients might spend more time with nurses or other providers who have less training than physicians. Some clinics are wedging more patients into a doctor’s day, plus adding email exchanges to their workloads. And there isn’t equal access for all: The wait times in rural areas, as well as for Medicaid patients and for visits with certain specialists, are likely to be longer.

“Health care is going through a transformation,” said Susan Skillman, deputy director of the University of Washington’s Center for Health Workforce Studies.

She doesn’t mean just the Affordable Care Act and the expanded insurance coverage that came with it. Many providers are trying to shift from the current “fee for service” model, which means paying for every doctor’s appointment, treatment and test, to “outcomes-based payments,” where doctors and clinics are rewarded for keeping or making patients healthy.

Collaboration

The hope is this transition encourages more-efficient medical care, such as using teams of health-care providers with different skills and a smarter use of technology. In the old model, no one gets paid for exchanging emails with patients, but if the goal is to make someone healthy and cut medical costs, electronic communications and telemedicine become more cost-effective tools.

At Group Health, a health-maintenance organization where the insurance and medical providers share a stake in cutting costs and providing good care, doctors have used email for years. In the past five, email use has become so popular that 60 percent of a physician’s interactions with patients each day are by email or phone.

“The patients love it,” said Dr. Paul Fletcher, Group Health’s medical director of primary care. Digital communication means there’s no copay, no appointments to schedule and patients don’t always have to trudge in to the office when feeling poorly.

At Group Health’s Northshore clinic in Bothell, patients seeing primary-care providers are cared for by a team that includes seven medical assistants, two licensed practical nurses, five registered nurses, one physician assistant, one advanced registered nurse practitioner (ARNP) and seven physicians. The nurses follow up for more routine problems, such as a bladder infection, or provide education for chronic conditions such as diabetes or high blood pressure. That frees up the more highly trained providers to do diagnosis and handle trickier care.

“We’re all very collaborative,” said Wendy Rychwalski, the ARNP at the Northshore clinic. The team meets each morning to review their patients and cases.

Providence Health & Services similarly uses teams of health-care educators and nurses to give ongoing support for patients with chronic diseases who need to manage their ailments outside of the doctor’s office.

“We’re working hard to redesign care,” said Dr. Craig Wright, senior vice president of physician services at Providence. “We think more and more about the primary-care team and not just the primary-care physician.”

Longer Medicaid waits

While local clinics report moderate wait times, independent sources suggest that’s not always the case. A national survey last year by health-care consulting firm Merritt Hawkins found that in Seattle there was a 23-day wait, on average, for family doctors.

And clinics primarily serving Medicaid recipients are getting hit harder. HealthPoint, with nine medical and six dental clinics in the Puget Sound region, has seen a 20 percent increase in new patients over last year.

The nonprofit center has opened two new clinics in recent years and expanded two others. Heather New, the newly insured patient, didn’t have any trouble getting care at HealthPoint’s Bothell clinic, which opened in 2012, but some of the more established locations have been so slammed they sometimes have been forced to turn new patients away, according to a spokeswoman.

Physician shortages

While clinics are squeezing more care out of the current system, it’s a limited fix.

Skillman’s team at the UW analyzed a state Office of Financial Management survey conducted in 2011 and 2012 of primary-care providers and found that 20 percent of them planned to retire in the next five years. Last year, she helped convene a health-workforce summit to talk about addressing the shortages.

The UW and Washington State University are both eager to ramp up their programs for teaching and training primary-care providers, particularly in Eastern Washington and more rural parts of the state where health-care shortages are chronic. In early July the state received $6.3 million in federal grants to boost residency training in areas with medically underserved populations, including Spokane, Yakima Valley and Tacoma.

In the meantime, there is a growing sense of urgency to train more providers, and fast.

“This is not just a local or regional issue. It’s a national issue,” said Dr. Jeff Bissey, associate medical director of primary care at The Everett Clinic. “We need to have more primary-care access, and that will take time.”

Â鶹ŮÓÅ Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at Â鶹ŮÓÅ—an independent source of health policy research, polling, and journalism. Learn more about .This <a target="_blank" href="/news/seattle-providers-mostly-keep-up-with-more-insured-but-worries-loom/">article</a> first appeared on <a target="_blank" href="">Â鶹ŮÓÅ Health News</a> and is republished here under a <a target="_blank" href=" Commons Attribution-NonCommercial-NoDerivatives 4.0 International License</a>.<img src="/wp-content/uploads/sites/8/2023/04/kffhealthnews-icon.png?w=150" style="width:1em;height:1em;margin-left:10px;">

<img id="republication-tracker-tool-source" src="/?republication-pixel=true&post=32545&ga4=G-J74WWTKFM0" style="width:1px;height:1px;">]]>This story was produced in partnership with

Washington state has blown past its targets for signing up new Medicaid participants under the Affordable Care Act (ACA).

The program’s ranks have grown roughly 25 percent in the past six months, helping fulfill one of the act’s key goals to provide health care to nearly all Americans.

By the end of March, more than 285,000 adults who are newly eligible to participate in Medicaid had signed up for coverage. That’s twice the number officials had hoped to reach by then, and a target they hadn’t expected to hit for three more years.

But with enrollment success comes the challenge of serving more people in a $10 billion program that’s already stretched thin in places.

Some of the new enrollees haven’t seen a doctor in years and need help navigating the health-care morass. Medicaid patients already struggle to get care in parts of the state and for certain medical specialties.

And while the hope is that more efficient, better care for all will drive down medical costs, they could still rise as more people are being helped.

Medicaid advocates acknowledge the hard work ahead but are committed to it.

“It’s the right thing to do,” said MaryAnne Lindeblad, Medicaid director at the state Health Care Authority, which oversees Washington Apple Health, the local name for the Medicaid program.

“Health care should be a right, not a privilege,” she said. “From that perspective, all folks ought to have access to a basic package of health-care services. It shouldn’t be based on income or need.”

Washington is one of 26 states where lawmakers voted to expand Medicaid coverage beginning Jan. 1 of this year. As part of the Affordable Care Act, federal funding will support that expansion.

Before then, Medicaid was available to low-income children and elderly people, pregnant women, people with certain disabilities, foster kids and as a temporary aid to the neediest families.

Poor, childless adults younger than 65 essentially were out of luck and had to rely on charity care.

Now people earning up to 138 percent of the federal poverty level can get free health and dental care. That covers individuals earning up to nearly $16,000 a year or a family of four making $32,500. Low-income people with higher wages must buy private insurance, though they would receive subsidies to reduce the cost.

Unaffordable

For Heather Hawley, health care has been a luxury beyond her financial means.

The 28-year-old SeaTac resident has worked in call centers, but the jobs rarely have included benefits, or the pay has been too low to afford insurance premiums. She has asked about government-funded health care, but nothing was available.

“You have to have a lot of kids,” she said. “And I’m not going to have kids just to get health benefits through the state.”

Hawley was laid off more than a year ago when her job answering calls for a bank’s reverse-mortgage program ended. She lives with her mom to save money.

“It’s tough times right now,” Hawley said. “There are so many people looking for the same job.”

Hawley has a promising lead with a department-store call center, but the benefits wouldn’t kick in for three months.

So she was thrilled to qualify now for Medicaid. She doesn’t have chronic health issues but wanted a backup plan beyond the emergency room, the default option for many uninsured people.

Two years ago, Hawley rushed to the ER when a bout of food poisoning resulted in her needing IV fluids. In December she was sick with bronchitis. It was a Saturday when her coughing got bad, Hawley said, and the ER “was the only place I could think of going.”

She was billed for the ER visits but doesn’t recall the amount and believes the bills have been sent to collection agencies.

The state and health-care providers hope to save money through Medicaid expansion by giving people like Hawley more cost-effective alternatives.

With better medical access, Medicaid supporters reason, people will seek more preventive medicine, such as vaccinations, and treat minor illnesses before they become severe. They’ll manage chronic conditions like high blood pressure and diabetes, forestalling emergency trips.

That should reduce the amount of free charity care hospitals provide, costs often passed on to insured patients through higher prices.

ER visits

While reducing ER visits may be one goal, a recent study from Oregon found that people newly enrolled in Medicaid actually used the ER more than other adults, potentially undermining one argument for savings. Some experts suggested the ER visits increased because the patients struggled to find doctors willing to take Medicaid insurance.

But a Washington state project that sought to reduce ER use by Medicaid recipients cut nearly $34 million in costs last year. And Washington leaders predicted expanding Medicaid would save the state $300 million in the first 18 months, mostly because of an influx of federal funding to cover health costs previously paid by the state.

That federal funding is a result of an ACA provision in which the feds pay 100 percent of the costs of newly eligible enrollees in states that expand Medicaid. Up to now, most Medicaid costs in Washington were split 50-50 with the federal government.

The 100 percent lasts three years, then ratchets down to 90 percent by 2020.

Meanwhile, the intensive enrollment outreach also recruited Medicaid-qualified people who hadn’t joined — an effect state officials had expected.

Some 138,000 of Washington’s new enrollees fall into this category, and their care will be matched at a lower rate — likely 50 percent — adding to the state’s financial burden. Last year, medical assistance for Medicaid enrollees cost on average $321 per person, per month.

Even with the higher match, 24 states have chosen not to expand Medicaid.

Savings to states

Studies show the expansion will save states money, in part by shifting costs to the federal budget, said Alan Weil, executive director of the nonpartisan National Academy for State Health Policy.

Academics and policymakers are interested in a more challenging question: Will Medicaid save money by reducing health costs?

But even before that answer emerges, Weil said, “we have a lot of evidence that people who have health insurance fair better, they’re healthier and live longer, and they’re more productive.”

Elizabeth Winders, manager of Medicaid programs at HealthPoint, a nonprofit with King County clinics, recalled one woman who hobbled on crutches into its Tukwila clinic. The woman had an accident, but wasn’t insured because her employer’s plan was too expensive. She had gone to the ER but couldn’t get needed follow-up care from a specialist. Her injury persisted and she lost her job.

When she enrolled in Medicaid, the woman told Winders: “ ‘This is going to change my life. I’m going to recover and get a new job. It’s hard to go to an interview on crutches and be someone they want to hire.’ ”

But even with Medicaid, the woman might have had trouble seeing a specialist.

Medicaid insurance generally pays doctors at a lower rate than Medicare and private insurance. To recruit and maintain Medicaid physicians, the ACA temporarily boosts the rate for primary-care doctors and services up to the level of Medicare.

Medicaid payments were so low that it required a 70 to 90 percent increase to reach Medicare rates, said Lindeblad, of the state Health Care Authority. The difference is being paid out of the federal budget.

The boost didn’t include specialists such as dermatologists and orthopedists.

22 cents on the dollar

The low reimbursements mean the specialists are earning 18 to 22 cents for every dollar they charge, said Sallie Neillie, executive director of Project Access Northwest, which helps uninsured and Medicaid patients find doctors. That’s compounded by uninsured and Medicaid patients being more likely to miss their appointments, she said.

State officials say they believe the Medicaid patients for the most part are finding care, and Molina Healthcare, a large Medicaid insurance provider, says it is increasing its network of primary-care doctors.

The state has crafted a multifaceted Health Care Innovation Plan designed to make health care more efficient and cost effective for those privately insured and those on government programs. A recent audit found that with better oversight of insurers covering Medicaid patients, the state could save by reducing overpayments.

Programs like Project Access Northwest offer a model for improving efficiency. The group assigns case managers to ensure patients get needed lab work, helps them get to appointments, and makes sure they do prescribed follow-up treatment.

Efforts to increase access include a greater use of nurse practitioners, giving scholarships for doctors who will practice in underserved areas, and opening more clinics targeted to low-income patients.

Because the greater goal isn’t simply an insurance card in every wallet. “People don’t want health insurance and health care,” said Sallie Thieme Sanford, a law and health services professor at the University of Washington. “They want to be healthy.”

Â鶹ŮÓÅ Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at Â鶹ŮÓÅ—an independent source of health policy research, polling, and journalism. Learn more about .This <a target="_blank" href="/medicaid/washington-state-medicaid-expansion/">article</a> first appeared on <a target="_blank" href="">Â鶹ŮÓÅ Health News</a> and is republished here under a <a target="_blank" href=" Commons Attribution-NonCommercial-NoDerivatives 4.0 International License</a>.<img src="/wp-content/uploads/sites/8/2023/04/kffhealthnews-icon.png?w=150" style="width:1em;height:1em;margin-left:10px;">

<img id="republication-tracker-tool-source" src="/?republication-pixel=true&post=32828&ga4=G-J74WWTKFM0" style="width:1px;height:1px;">]]>This story was produced in collaboration withÂ

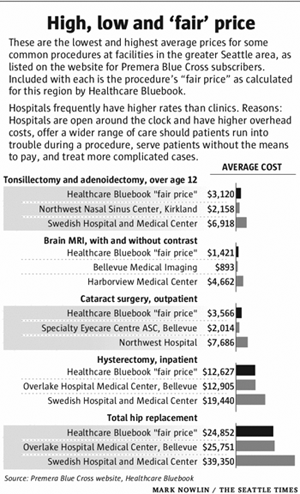

What if you had a headache that wouldn’t go away? At the area’s top trauma center, a brain MRI will cost more than $4,600, while an imaging center on the Eastside will charge $900.

Need your tonsils out? A Kirkland nasal-and-sinus clinic will charge you $2,200, but the surgery will be nearly $7,000 at a Seattle hospital. Which would you choose?

A prime objective of the Affordable Care Act is to bring down America’s health-care costs, which are the highest per person in the world. But how can the U.S. shrink its medical bills if patients are almost always buying health care with no idea what it costs?

Washington has been able to do little to shed light on health-care costs, and the state last year earned an “F ” for its cost-transparency laws, according to groups promoting health-care reform.

That soon could change.

Gov. Jay Inslee and some state lawmakers are pushing for new rules that would create a database listing hundreds of medical procedures, what they will cost at clinics and hospitals statewide, and information about the quality of the medical providers.

“We made a decision with the Affordable Care Act to use competition to control costs,” said Bob Crittenden, Inslee’s senior health-policy adviser. “Competition requires a number of things. You need enough information to make decisions, and we don’t have that right now.”

The proposal has backing from many big players in medicine and business, but the support is not universal. The state’s largest insurance companies — Regence Blue Shield and Premera Blue Cross — oppose requirements to share the treatment prices they’ve privately negotiated with clinics and hospitals.

There’s also the challenge of pairing cost data with information about the quality of a doctor or hospital. After all, who wants the cheapest physician if he’s also the worst?

And there are questions whether transparency can drive down prices. Hospitals and clinics have been consolidating, creating fewer, bigger companies and less competition. Lifesaving drugs and treatments might be available from only one company or location, giving patients little choice.

The biggest question is whether patients will seek this information and use it to shop more wisely. Transparency supporters think the public is ready for them to pull back the curtain on cost and quality.

“More information will beget more curiosity,” said Mary McWilliams, executive director of the Washington Health Alliance, a nonprofit that has earned national kudos for tracking the quality of health-care delivery.

“I think people have assumed it’s all the same quality and all the same cost,” she said. “Getting them to recognize that it’s not all the same is the first threshold.”

“Huge price variation”

When Jeff Rice was dinged $200 for cholesterol blood work that should have cost $20, the Tennessee-based physician turned his frustration into a business opportunity.

In 2008, Rice launched Healthcare Bluebook, a company that collects data on what insurance companies pay for medical care, then calculates a “fair price” for procedures from allergy tests to heart surgery. Consumers can search for prices for free online and use the information as a benchmark to shop around.

“Many patients don’t know there is this huge price variation,” Rice said.

There are other transparency tools available, but all have their limitations. Many insurance companies have online cost-comparison tools for their customers. A recent search on the Aetna site found prices for roughly 30 common procedures, while Regence lists prices for 350 services.

On the quality side, the Washington Health Alliance publishes “Community Checkup Report,” which evaluates the quality of doctors, clinics and hospitals. The national Leapfrog Group scores hospitals.

In coming months, lawmakers in Olympia will consider various proposals to expand and greatly improve such transparency. One bill would require insurance companies to enhance their shopping tools to include price and quality information side-by-side.

Recent hearing

A more controversial proposal would create an “All-Payer Claims Database.” Hospitals and clinics have a “billed” rate for services, but insurance companies negotiate lower “allowed” rates, the amount they agree to actually pay for a procedure. The legislation would require payers — mostly insurance companies — to reveal what they are spending on services at different locations, so the data could be compiled into a database available to everyone.

At a recent hearing for the bill, representatives from the Washington State Hospital Association, Washington State Medical Association, Seattle Metropolitan Chamber of Commerce and the National Federation of Independent Business all testified in support of creating the database.

Only Regence and Premera officials spoke against it.

The insurance companies carefully guard the rates they negotiate. They consider it proprietary information they are not keen to share with competitors, health-care providers and others.

“We simply do not believe that [the All-Payer Claims Database] has any history of demonstrating any meaningful cost or quality improvement,” said Premera’s Len Sorrin, at the hearing.

The companies do, however, support cost tools for their own customers. A spokesman for Regence testified that searching for prices drives patients to lower-cost options.

Databases in 11 states

So far, at least 11 states have created these databases in various forms, and many more are interested. Most of the databases were built in 2008 or later, and there’s little information on their effects on costs or quality.

But the world of health insurance is changing. Deductibles — the amount a patient must pay before an insurance company starts covering medical bills — are going up. More than one-third of insured workers have deductibles of $1,000 or more, and many plans also have “coinsurance,” which sets a percentage of medical bills patients must pay even if they’ve reached their deductible cap.

Gone are the days of visiting the doctor and paying a $15 copay. Patients are more frequently footing the bill.

“When it’s your money, you ask a lot more questions about what things cost,” said Rice, the founder of Bluebook.

But shopping for health care can be more complicated than buying other essentials.

Transparency supporters like to illustrate the influence of price by comparing it with buying gasoline. Most drivers check the posted per-gallon price before filling up. If one station offered gas at $4 a gallon, they would drive past the pump offering it for $20 a gallon — a degree of price difference seen in some medical services.

But is that the right metaphor? What if you’re driving on fumes and there’s no other pump for miles around? When you’re a desperate shopper, chances are you’ll pony up if you can.

Challenges, limitations

Some argue that by publishing the cost information, the cheaper locations will raise their prices rather than the expensive sites dropping theirs. Douglas Conrad, a professor in the University of Washington’s School of Public Health, called that argument a red herring. Over time, he said, the prices come down, whether through market forces or action by antitrust authorities.

The relationships patients develop with their doctors pose potentially more difficult complications.

Conrad acknowledges the challenges and limitations to how much influence transparency can exert on the health-care system, but he thinks it can make a positive difference.

“If price and quality information get out there, and there is a push by the state to force transparency where it’s been difficult to get … that could change things,” Conrad said. “The promise is there.”

Â鶹ŮÓÅ Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at Â鶹ŮÓÅ—an independent source of health policy research, polling, and journalism. Learn more about .This <a target="_blank" href="/news/washington-state-lawmakers-looking-to-lift-veil-on-health-care-prices/">article</a> first appeared on <a target="_blank" href="">Â鶹ŮÓÅ Health News</a> and is republished here under a <a target="_blank" href=" Commons Attribution-NonCommercial-NoDerivatives 4.0 International License</a>.<img src="/wp-content/uploads/sites/8/2023/04/kffhealthnews-icon.png?w=150" style="width:1em;height:1em;margin-left:10px;">

<img id="republication-tracker-tool-source" src="/?republication-pixel=true&post=33297&ga4=G-J74WWTKFM0" style="width:1px;height:1px;">]]>This story was produced in partnership with

Worried that too few young people are signing up for health insurance, Washington state officials are stepping up their efforts to get buy-in from the crucial demographic.

On Wednesday, they launched a campaign with Live Nation, a global concert promoter, in the hope that young adults will accept a dose of health-care education along with performances by their favorite artists.

The goal of the Live Nation partnership is to tell young adults, “there’s a new way to get insurance, and there are ways to address some of the cost concerns that they’ve had in the past,” Marchand said.

Kevin Wren, 29, a baker at Homegrown Bakery in Seattle, said signing up on the state exchange was “not that difficult” (Photo by Greg Gilbert/Seattle Times).

The campaign will include a contest through the exchange’s Facebook page to win tickets to the popular Sasquatch! Music Festival, educational booths at upcoming shows, including Justin Timberlake’s KeyArena concert, and information shared through email and social-media sites. Those efforts come on top of other outreach strategies taking place on college campuses and through doorbell ringing campaigns.

Nationwide, Affordable Care Act supporters say young adults are critical to the success of the health-care overhaul. Younger people are typically healthier and require less medical care, so their insurance premiums more than cover their medical needs. That leaves the unspent dollars from their premiums to subsidize the costs of treating older, sicker people.

In Washington, 18- to 34-year-olds make up roughly half of the uninsured population. But so far they represent only 20 percent of those enrolled in Washington Healthplanfinder, the state’s new insurance exchange. Nationally, 24 percent of enrollees are young adults, according to data released this week.

Obamacare supporters have until the end of March, when open enrollment ends, to boost the number of “young invincibles” — so called because they perceive themselves as invulnerable to injury and disease.

“The main reason they’re not insured is they’ve thought it’s something they can’t afford,” said Michael Marchand, spokesman for the Washington exchange. Most insurance sold on the exchange is subsidized through federal tax breaks, based on a person’s income level.

Many experts warn that if too few young people sign up — the goal nationally is for 40 percent of enrollees to be 18- to-34-years-old — that health-care costs could climb, leading to higher premiums for everyone and threatening the success of the state marketplace.

But getting 18- to 34-year-olds signed up might be trickier than expected, and some researchers wonder if more attention needs to be paid to enrolling healthy people of all ages to keep down insurance costs.

“Invincible”? Not all

At 29, Seattle’s Kevin Wren is one of the young adults already on board.

In October, Wren lost his health benefits when he was laid off from a public-relations job. Now he’s a baker at a cafe called Homegrown, but the job didn’t come with insurance. Wren knew about the Affordable Care Act and checked out the state’s website.

“There is a lot of confusion out there, but if people are willing to sign up, it’s not that difficult,” he said. Based on his income, Wren qualified for a subsidy and is now enrolled in a plan with Group Health Cooperative that costs him $86 a month.

While Wren is young, he’s also proof that no one is invincible. About 15 years ago he was diagnosed with Type I diabetes, which his dad also has. Wren needs multiple doses of insulin to stabilize his blood-sugar levels each day, at a cost of $600 a month.

Wren recounts a time after graduating from college when he was unemployed and without benefits. He ran low of insulin and had to tap his dad’s supply, rationing the doses as best he could. After signing up for insurance, Wren persuaded a work colleague to do the same.

“A lot of young people don’t have chronic conditions,” he said. “If they’re well, they’re kind of fair weather that way.”

National surveys have tried to determine young people’s attitudes about insurance. Approximately three-quarters of Americans age 18 to 30 say health insurance is something they need. And about two-thirds worry about paying medical bills, according to a June 2013 survey by Kaiser Family Foundation.

This fall, University of Washington graduate students interviewed a dozen young adults about their health-care opinions. Many recalled going to the doctor or hospital and being hit with large, unexpected bills afterward. They doubted that private insurance companies were offering affordable, desirable plans. Many wished for a single-payer system.

“They have a lot of emotional and very rational reasons for feeling skeptical about insurance and the worth of it,” said Louisa Edgerly, an adjunct professor with the University of Washington’s Department of Communications. “That makes for a more complicated conversation around these decisions about whether to purchase or not purchase a plan.”

From the interviews, the students produced short videos that soon will be posted on university websites and used to lead discussions at coffee shops, libraries and other venues. The videos don’t cheerlead the Affordable Care Act, Edgerly said, but offer an authentic message about health-care concerns while still ultimately encouraging young people to enroll.

Some doubt the focus

Recently, some experts have challenged the focus on young adults and the idea that Obamacare costs will spiral out of control if fewer sign up than hoped for.

That’s in part because insurance premiums vary widely according to age. The same plan that costs a 20-year-old $150 will cost a 50-year-old $425. That means a healthy, middle-aged person could be more economically beneficial to the program than a less-well young person.

In part because of this age-based disparity in premiums, an analysis released last month by researchers with Kaiser concluded: “Enrollment of young adults is important, but not as important as conventional wisdom suggests.”

Marchand, of the state’s insurance exchange, is not giving up on young adults.

“It’s still going to be mission critical that we get this population captured for enrollment targets that we have as a state,” he said. The goal is to sign up 280,000 people in the exchange by the end of the year.

So far, more than 73,000 have enrolled and paid for coverage.

Â鶹ŮÓÅ Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at Â鶹ŮÓÅ—an independent source of health policy research, polling, and journalism. Learn more about .This <a target="_blank" href="/insurance/washington-state-woos-young-invincibles/">article</a> first appeared on <a target="_blank" href="">Â鶹ŮÓÅ Health News</a> and is republished here under a <a target="_blank" href=" Commons Attribution-NonCommercial-NoDerivatives 4.0 International License</a>.<img src="/wp-content/uploads/sites/8/2023/04/kffhealthnews-icon.png?w=150" style="width:1em;height:1em;margin-left:10px;">

<img id="republication-tracker-tool-source" src="/?republication-pixel=true&post=34053&ga4=G-J74WWTKFM0" style="width:1px;height:1px;">]]>This story was produced in partnership with

If you want to know whether people in Washington state like or loathe Obamacare, you could just ask them which political party they prefer.

That’s because 80 percent of Democrats surveyed approve of health-care reform while 80 percent of Republicans don’t, according to an Elway Poll of Washington voters conducted on behalf of The Seattle Times. Independent voters are the wild card, with 41 percent in favor and 46 percent against the overhaul, formally known as the Affordable Care Act.

The Elway survey of 406 Washington voters earlier this month asked about their personal experiences with health care and their opinion of the Affordable Care Act (ACA), which kicks into high gear Oct. 1 with the launch of insurance marketplaces called exchanges.

Overall, blue-leaning Washingtonians in the survey view Obamacare more favorably than Americans as a whole, as measured by a recent national Gallup poll.

Red, blue or independent, we all get sick and see the doctor now and then. What makes the health-care act so politically polarizing — as exemplified by a move last week by U.S. House Republicans to strip funding for the act?

“Each side has a reason,” said William Rorabaugh, a history professor at the University of Washington. “It’s not just ideology.”

Republicans don’t like the reform for many reasons: the provision requiring people and businesses to buy health insurance; concerns that medical costs will continue to soar while the quality of care declines; its expansion of entitlements; and the belief that it trumps personal freedom while giving the federal government too much control over health-care decisions.

Democrats, on the other hand, might not love every feature of the Affordable Care Act, but many support it for bringing medical care to more people.

“The issue has been in Democratic Party circles for a long time,” Rorabaugh said.

“This is the last big missing piece of social legislation,” he said. If you look at democracies worldwide, they all have free education, retirement and welfare systems, and — except for America — national health care.

The health-insurance exchanges opening next month — including this state’s Washington Healthplanfinder — will sign up the uninsured and provide new policy options for people who aren’t covered by an employer. The ultimate goal of Obamacare is for most everyone to either have health insurance or have coverage under a federal program such as Medicare, Medicaid or the military.

The plan is for health-care costs to come down. That happens by paying for preventive medical treatments, shifting to a system that rewards doctors and hospitals that actually make people well rather than those that provide the most procedures, and expanding the pool of who is insured — in part by adding more young and healthy people.

The challenge of enrolling the uninsured will be easier in this state than in many other places. In Washington, 45 percent of those surveyed in the Elway poll approve of the overhaul, while 41 percent of Americans overall like the changes. On the flip side, 42 percent of voters here disapprove of the law while 49 percent of the U.S. population do, according to an August poll by Gallup.

The Elway poll, conducted Sept. 3-5, has a margin of error of plus or minus 5 percent.

The poll also found:

•While the ACA is the biggest overhaul of American health policy since Medicare began in 1965, almost half of the people surveyed said it either won’t make much difference in their lives, or they don’t know whether it will.

• Slightly more than half of the people who say they are familiar with the ACA also say they approve of it. The approval rating is 38 percent among those who say they are unfamiliar with it.

• Forty-one percent of people in households earning $50,000 or less annually approve of the ACA, while 58 percent of respondents in households making $100,000 or more say they like Obamacare.

• The people who will likely feel the biggest impact of the new insurance exchanges — those who are currently uninsured or have individual insurance — are also those who least like the ACA, with 37 percent in favor and 47 percent disapproving.

Strong feelings about purchase requirement

Carol Sterling is among those who are uninsured. The single mom from Lynnwood could get insurance through the nursing facility where she works, but she can’t afford her share of the premium. Sterling’s two children get insurance coverage through their dad.

“I can pay for my rent and make sure my kids have food on the table, or I have insurance,” Sterling said. “There are no two ways about it, my kids come first.”

Sterling, 42, says she’s in excellent health. She said her own health-care knowledge, combined with that of family members who also work in medicine, provides the information she needs to stay healthy and treat some ailments.